How Trafigura buys the silence of its ex-employees

Adrià Budry Carbó, 5 december 2024

©

Tommy Trenchard / Panos Pictures

©

Tommy Trenchard / Panos Pictures

“Erase – All ConsultCo”. This simple note was written by hand in a notebook. Someone at Trafigura had just launched the big clean-up operation. And the man, nicknamed called “Mr Non-Compliant” for his ability to do “things that could not be done internally within the group”, was about to execute just that. From his discreet trustee office in Geneva’s rue de la Croix d’Or, he was the man behind the trading house’s secret commission-accounting system.

The “controller” sometimes also had to erase the traces of his work, as highlighted by the note found by the federal judicial police during their search of the trustee office. This is where they found the information relating to an offshore company – ConsultCo Trading Ltd., used by T.P., an ex-employee of Trafigura (1995-2002), who became its intermediary, to allegedly pay bribes, between 2009 and 2011, to a senior Angolan official in exchange for favourable contracts.

©

Tommy Trenchard / Panos Pictures

©

Tommy Trenchard / Panos Pictures

Read the report: Despite corruption trial, Trafigura still in the driver’s seat

Trafigura’s executives are under pressure. Ever since Mariano Marcondes Ferraz was arrested in Brazil in 2016, the vice has been tightening. The former Trafigura executive made a confession in exchange for a reduction of his 10-year prison sentence. He admitted that bribes were paid on behalf of the trading house in connection with the Petrobras scandal, but also in Angola. The Office of the Attorney General of Switzerland (OAG) launched an investigation in July 2020. The Federal Judicial Police conducted several searches in the offices of Trafigura and two other companies (April and September 2021), as well as in those of “Mr Non-Compliant”’s trustee office (September 2022).

Trafigura’s trial for bribery of a foreign public official before the Federal Criminal Court began on 2nd December 2024 in Bellinzona, Switzerland. In the dock alongside the multinational are three individuals: the Angolan civil servant, the owner of ConsultCo Trading Ltd (T.P.) and Michael Wainwright, one of Trafigura’s most senior executives. This is the first time this scenario has been played out.

The carrot and the clawback

They might have been one of the largest trading houses in the world – a $244 billion turnover for 12,000 employees – and been well-versed in carrying out operations on the fringes of the law; but when you act in haste, you make mistakes. So, when Trafigura didn’t try to cover its tracks, it handsomely compensated those who were supposed to remain silent.

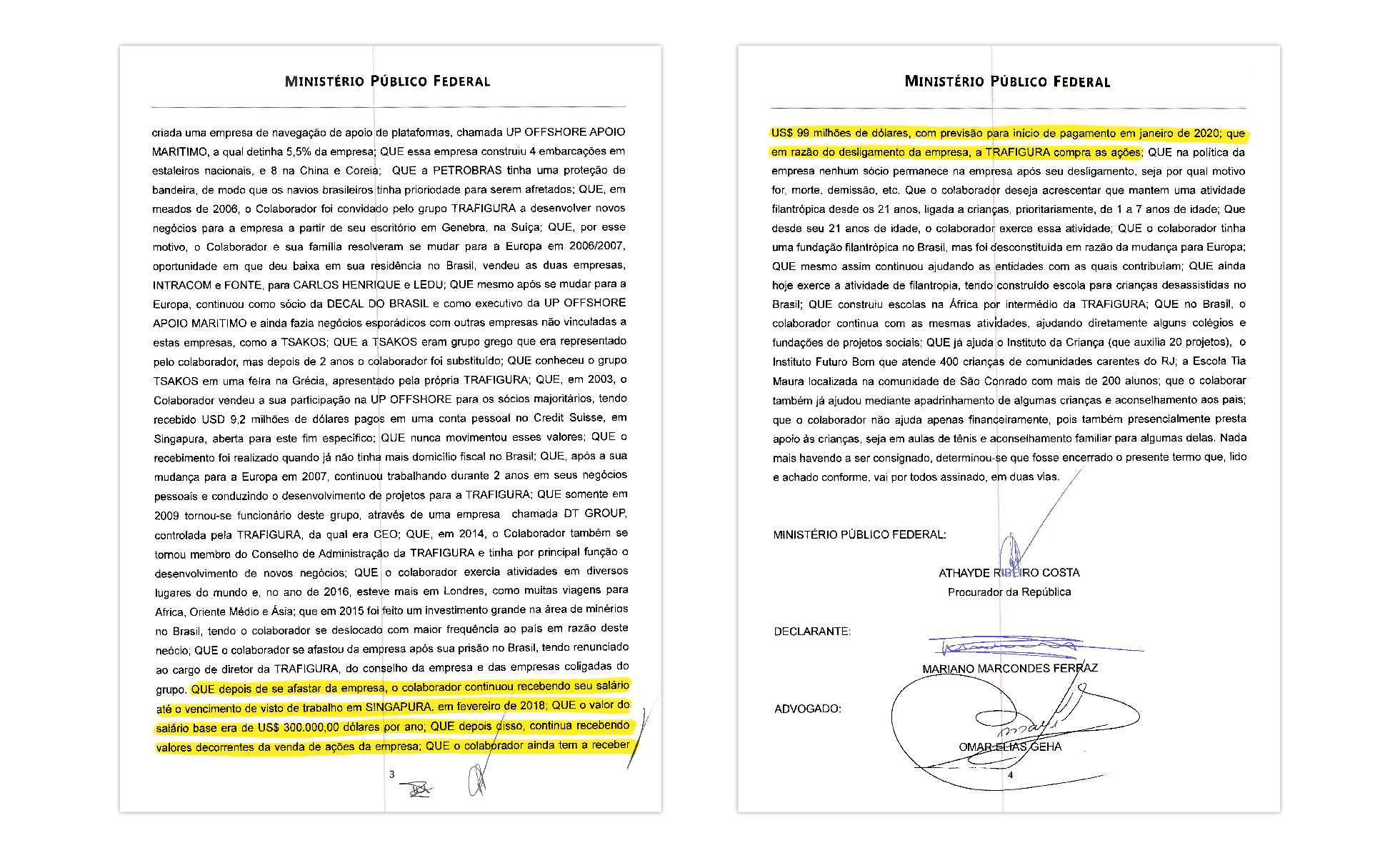

In May 2019, Mariano Marcondes Ferraz stated – as part of his “cooperation agreement” with the Brazilian justice system in May 2019 – that he received an annual salary of $300,000 at Trafigura. Not forgetting future payments coming to him, staggered from January 2020, for a total amount of $99 million, equivalent to the value of the shares still held by this former member of Trafigura’s board of directors.

In a similar manner to other trading houses, Trafigura’s is owned by its senior executives. Some 1,400 shareholders share the billions in profits generated by the multinational ($1.7 billion in 2022, $5.9 billion in 2023). When they retire, die or are made redundant, they still hold a stake in Trafigura or one of its Maltese or Caribbean subsidiaries (the register of shareholders is a real Trafigura Who’s Who). The procedure for buying back their shares is organised by Trafigura according to timetable, spread over several years.

This has the two-fold benefit of closely linking Trafigura’s executives with the company’s performance and deterring any criticism. Last June, Reuters disclosed the existence of a letter from management, sent to both current and former employees, threatening to cut these payments in the event of “any breaches of confidentiality”. These “clawback” clauses are typically used by financial groups that demand repayment of a bonus in the event of misconduct or poor performance.

Between 2017 and 2020, Trafigura even asked its employees to sign non-disclosure clauses preventing them from communicating with judicial authorities. In particular, the Commodity Futures Trading Commission – the body that regulates derivatives markets in the US – imposed a fine of $55 million on it in June 2024 for these practices, as well as for fraud and market manipulation.

Michael Wainwright, former COO of Trafigura, was in charge of planning the clawbacks over years and, therefore, of implementing the code of “omertà” within the trading house. When the trial was announced, the man who held the group’s purse strings – with a reputation for being meticulous and aloof – was given early retirement by Trafigura, at the age of 51. During his hearing on 6th June 2023, the minutes of which were seen by Public Eye, Mariano Marcondes Ferraz referred to his share buybacks being blocked by Michael Wainwright and the rest of the board of directors, to whom he sent messages, asking whether “the payments were going to come or not”.

Concrete benefits

But back to ConsultCo Trading Ltd: this name provides a screen for covering up Trafigura’s entire secret accounting system. It facilitated the job of the trading house’s intermediaries (this type of service is outsourced, for obvious reasons) in paying commissions to the managers of state oil companies. This company domiciled in the British Virgin Islands also owned a share in Trafigura via two Maltese entities, shareholders of the Puma Energy subsidiary (PE Investments Ltd and Global PE Investors Plc). Hence the “Erase - All ConsultCo” note, as everything had to disappear. The share buyback was completed in September and October 2022 – for an unknown amount.

However, the owner of ConsultCo Trading Ltd – a prominent figure from Geneva who owns a port on the lake’s left bank – was allocated assets by Trafigura, seven months after the OAG’s investigation was opened. In February 2021, the Puma Energy subsidiary sold its entire stake in the Congolese company SPSA Cobil SA to an entity called Translog Sàrl, owned by T.P., together with his Congolese partner G.M., according to official documents that we have been able to access.

Via Translog, T.P. already held shares in SPSA Cobil SA. The company operates oil storage terminals in Matadi, strategically located on the Congo River. Thanks to his contacts with the son of the President of the Republic of Congo, Denis Christel Sassou-Nguesso, the Trafigura intermediary obtained crude oil, converted into fuel – at a “discount price”, as expressed by Africa Intelligence – by the state refineries Coraf, and then sold on the other side of the river in the densely populated DRC. The system is described in the industry as a “cash machine”.

Why did Trafigura divest itself of SPSA Cobil SA? Was this transfer of assets a reward for services rendered, and if so, what kind of services? When contacted, the Geneva based trading house had “no comment to make on [our] questions”. Which is just another way of preaching silence.